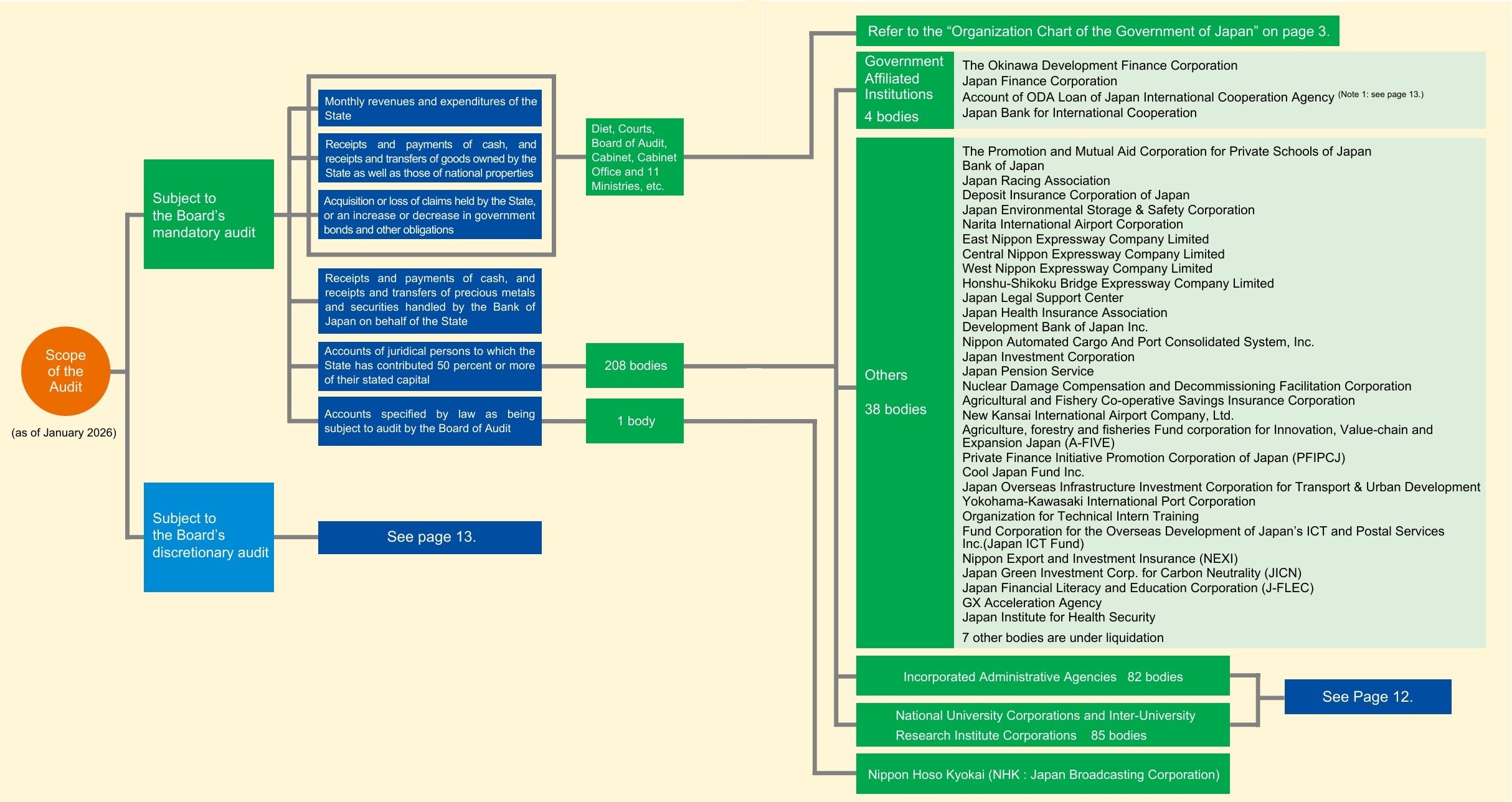

Those which are subject to audit by the Board are classified into two categories, i) those which the Board must audit regularly (mandatory audit subject) and ii) those which the Board may audit when the Board finds it necessary (discretionary audit subject), ranging from the whole of State accounts to entities whose stated capital has been contributed by the State and prefectures, municipalities and other organizations as grantees of subsidies and other financial assistance from the State.

To conduct an audit of those which are subject to the Board’s discretionary audit, an Audit Commission decision is required. The Board notifies such decision to the relevant auditees.