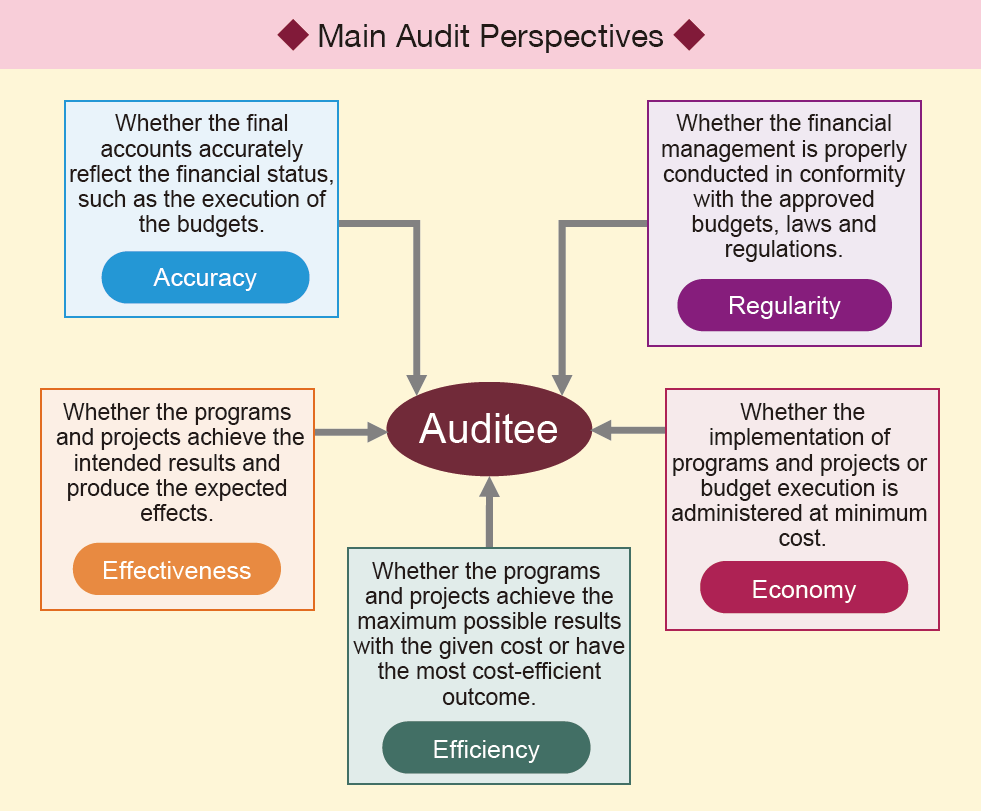

The Board conducts audits with broad and diverse perspectives.

The Board conducts audits with such perspectives as i) whether the final accounts

accurately reflect the financial status such as the execution of the budgets

(Accuracy); ii) whether the financial management is properly conducted

in conformity with the approved budgets, laws and regulations

(Regularity); iii) whether the implementation of programs and projects

or budget execution is administered at minimum cost (Economy); iv)

whether the programs and projects achieve the maximum possible results with the given

cost or have the most cost-efficient outcome (Efficiency); and v)

whether the programs and projects achieve the intended results and produce the expected

effects (Effectiveness).

The audit with the perspectives of Economy, Efficiency and Effectiveness is collectively

called the ‘3E audit’, derived from the initial letters of each word.