Analysis and Review of Audit Findings

Audit findings by the Board demonstrate criticism to the auditees and are to be informative to other institutions to be audited and the nation. As such, misjudgment should be avoided.

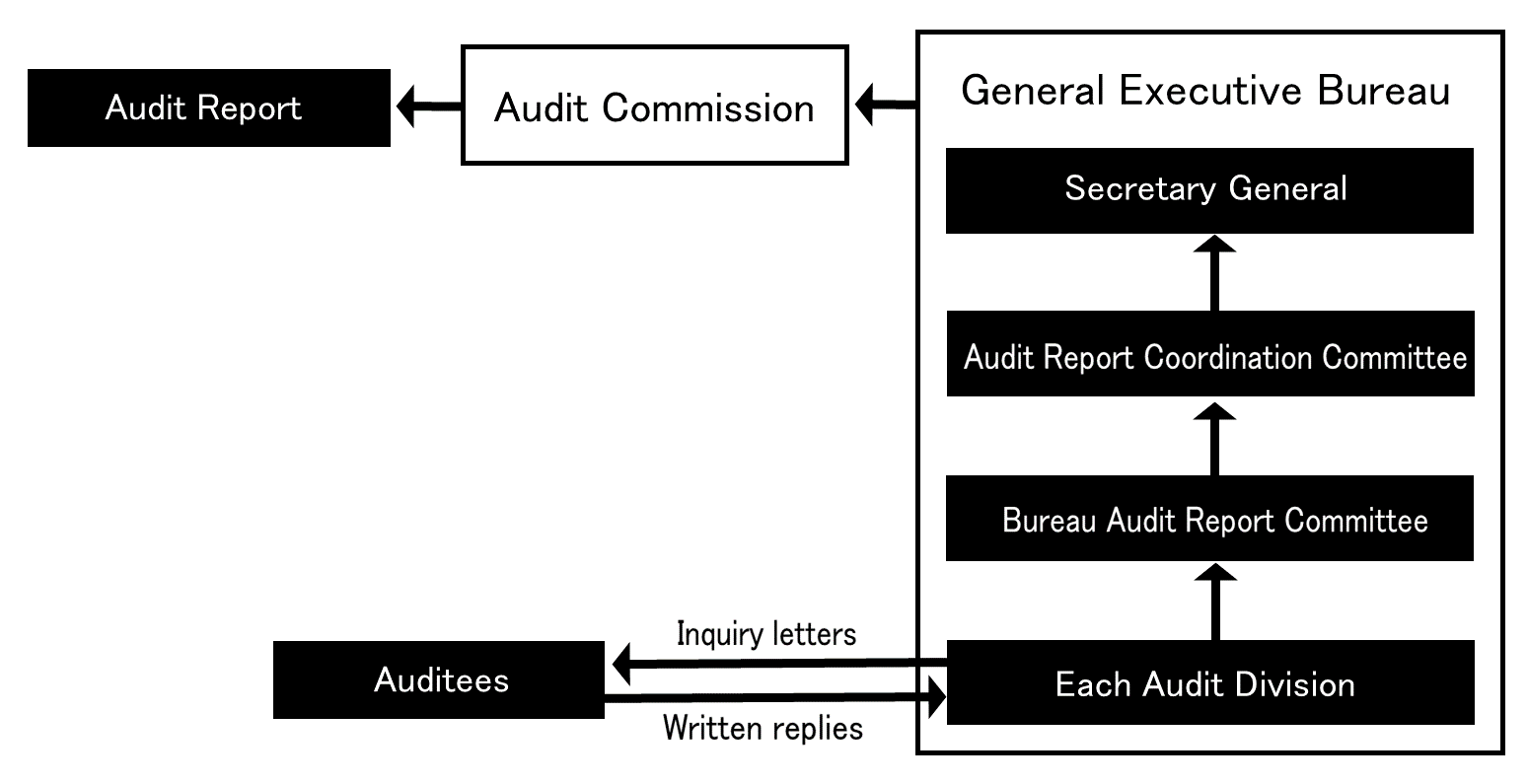

If any improper financial management comes to light in the course of audit, the Board takes the following procedures to confirm the situation, in addition to double-checking and ample analysis of the causes and remedial measures.

(1) Inquiry letters to the auditees

As for any improper or unreasonable financial management found in the course of audit, the Board sends inquiry letters to those who are responsible in each auditee.

These inquiry letters describe the outline of improper financial management, related questions, tentative evaluation and reasoning, in order to confirm the facts and views of auditees and to clarify any questions.

The Board examines the situation by requesting written auditee replies to the inquiry letters.

(2) Request for relevant information and/or technical appraisal from third parties

In dealing with highly technical issues, there are cases in which the Board’s own staff alone cannot make a fair decision. In such cases, the Board asks independent professional organizations or other experts for their professional views or opinions, and makes its final judgment with due consideration to their views or opinions.

If any improper or unreasonable financial management is found as a result of thorough analysis and review of the audit findings, the Board presents its opinions to, or demands measures from the auditees, or reports them in the Audit Report as, for example, matters that the Board has identified as being in violation of laws and regulations or the approved budget, or as being improper.

The final judgment is made by the Audit Commission, a decision-making body of the Board, after due deliberation with sufficient care in order to avoid misjudgment.

Composition and operation of the Committees and deliberations are as follows.

【Committee Structure】

Each bureau establishes a Bureau Audit Report Committee composed mainly of the Director General of each bureau (as a chairperson) and Senior Directors of each bureau. The Secretariat sets up the Audit Report Coordination Committee composed of the Deputy Secretary General (as a chairperson) and Senior Directors of the Secretariat.

【Deliberation】

Deliberation is conducted on various aspects such as 1) correct understanding of the facts, 2) analysis of the system and application of the laws and regulations, 3) consideration of relevant past circumstances and changing situations and 4) analysis of the causes and remedial measures.

【Adoption of Peer Review System】

Both the Bureau Audit Report Committee and the Audit Report Coordination Committee adopt a peer review system for securing objectivity and credibility of their judgment. In the system, each audit case is reviewed critically in advance by one of the members in each Committee regarding the accuracy of the description of facts and relevance of the conclusion, and the result of the review is reported to the relevant Committee.