Audit Practice

Audits are divided into two types: in-office audit and field audit.

(1) In-office audit

The Board continuously conducts in-office audit by:

1. Checking the contents of documents such as statements of accounts, which show the numeric results of financial management of each entity, as well as supporting documentary evidence including contract documents, invoices and receipts, submitted by auditees in accordance with the Regulations on the Submission of Accounts established by the Board. (Refer to the "Statements of Accounts and Documentary Evidence" below.)

2. Having auditees submit materials and data on the implementation of projects in order to check the contents, and by interviewing relevant persons using an information communication system.

Documentary evidence stored at the Board

Interview using a web conferencing system

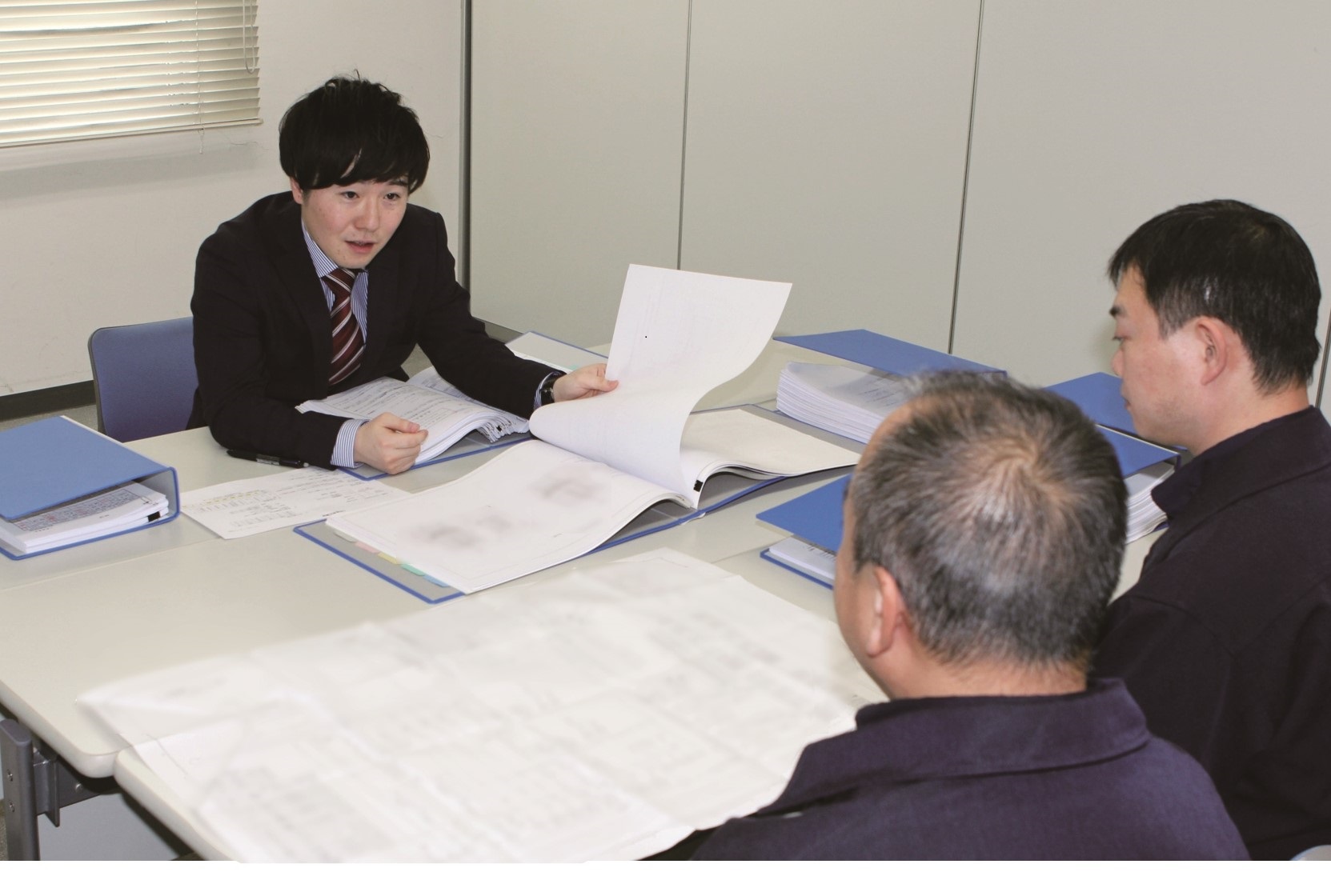

(2) Field audit

Information which can be obtained from the statements of accounts and documentary evidence submitted to the Board is limited and not always enough to determine the adequacy of financial management or projects implementation.

The Board, therefore, dispatches its auditors to the headquarters and branches of ministries and government agencies, or project sites to conduct field audits. As for local governments that carry out various projects with State subsidies, the Board also conducts field audits to examine whether the subsidies have been used properly. The Board also dispatches staff to various overseas locations such as ODA project sites and the diplomatic missions for audit work.

Sites to be audited are selected by taking into consideration priority audit issues and human resource allocation determined by the Audit Plan, results of the in-office audit, frequency and results of past audits, deliberations in the Diet, and information from the media or public.

In the field audits, auditors examine the actual conditions of administrative work and projects by checking accounting books as well as documentary evidence which is retained by the auditees, interviewing the officials in charge and other relevant persons, observing property management, and inspecting completed physical works.

Most audit findings reported in the Audit Report are brought to light through the field audits, which are of great importance in the audits conducted by the Board.

(Note) The photos below were taken before the COVID-19 pandemic.

(At the airport facility)

(At the Japan Self-Defense Force Base)

(At the auditee’s office)

(In the medical facility)